Singapore trust formation is the process of legally establishing a trust arrangement where a trustee holds and manages assets on behalf of beneficiaries under Singapore law. Three parties define every valid trust: the settlor, who creates and funds the trust; the trustee, who holds legal title to the assets; and the beneficiaries, who hold the beneficial interests. The governing legislation includes the Trustees Act, the Trust Companies Act 2005, the Civil Law Act 1909, and the Conveyancing and Law of Property Act 1886. Getting the structure right from the outset determines whether the trust is legally enforceable or void from inception.

What are the legal requirements to create a valid trust in Singapore?

An express trust must satisfy three certainties to be legally valid in Singapore: certainty of intention, certainty of subject matter, and certainty of objects. This standard, recognized by the Ministry of Law, is the single most critical threshold in Singapore trust law basics. Without all three, no beneficial interest arises, regardless of how formally the documents are drafted.

The three certainties work as follows:

- Certainty of intention: The settlor must clearly intend to create a trust, not merely express a moral wish or impose a personal obligation. Courts look at the language of the trust deed and surrounding circumstances to determine genuine intent.

- Certainty of subject matter: The trust property must be precisely identified. Vague descriptions such as "some of my assets" or "a portion of my estate" fail this test and can render the trust void.

- Certainty of objects: The beneficiaries must be identifiable with sufficient certainty. For fixed trusts, each beneficiary must be individually ascertainable. For discretionary trusts, the class of potential beneficiaries must be defined clearly enough for a court to determine whether any given person qualifies.

Beyond the three certainties, specific asset types carry additional formal requirements. Trusts over immovable property require a written declaration signed by an authorized person and a separate conveyance of the property by deed in English, under Civil Law Act 1909 section 7 and Conveyancing and Law of Property Act 1886 section 53. This means signing a trust deed alone is legally insufficient for real estate. A separate English-language conveyance deed must transfer the property to the trustee before the trust becomes enforceable.

Pro Tip: Have a qualified Singapore lawyer review the trust deed before execution. A single ambiguous phrase in the subject matter clause can trigger a court challenge years later, at significant cost to the estate.

How to choose and appoint trustees for a Singapore trust

Trustee selection is one of the most consequential decisions in the trust formation process. Singapore law recognizes three categories of trustees:

- Individual trustees: Private individuals, including family members or close associates of the settlor. They hold legal title and manage assets per the trust deed, but they carry full personal fiduciary liability and may lack the technical expertise required for complex trust administration.

- Licensed Trust Companies (LTCs): Regulated entities approved by the Monetary Authority of Singapore (MAS) under the Trust Companies Act 2005. Licensed Trust Companies can act as trustees and provide full trust administration services, including Anti-Money Laundering and Countering the Financing of Terrorism (AML/CFT) compliance checks.

- Private Trust Companies (PTCs): Entities set up specifically to act as trustee for a single family or group of related trusts. PTCs must engage a Licensed Trust Company to perform AML/CFT functions, which adds a layer of regulatory oversight without requiring the PTC itself to hold a full MAS license.

Trust businesses in Singapore must be licensed and regulated by MAS under the Trust Companies Act unless a specific exemption applies. Operating a trust business without a license or valid exemption is a criminal offense under section 3 of the Act. MAS holds powers to approve controllers, supervise operations, and enforce compliance across all licensed entities.

Trustees carry significant legal obligations under the Trustees Act. Fiduciary duties include acting in the best interests of beneficiaries, managing assets responsibly, maintaining proper records, and avoiding conflicts of interest. Breach of these duties exposes trustees to personal liability, including surcharge for losses caused to the trust estate.

Beyond the trustee, settlors may appoint a protector to provide an additional layer of governance. A protector may be appointed to supervise trustees and exercise veto or authorization powers as specified in the trust deed. Protectors are particularly useful in family trusts where the settlor wants ongoing influence over major decisions without retaining legal ownership of the assets.

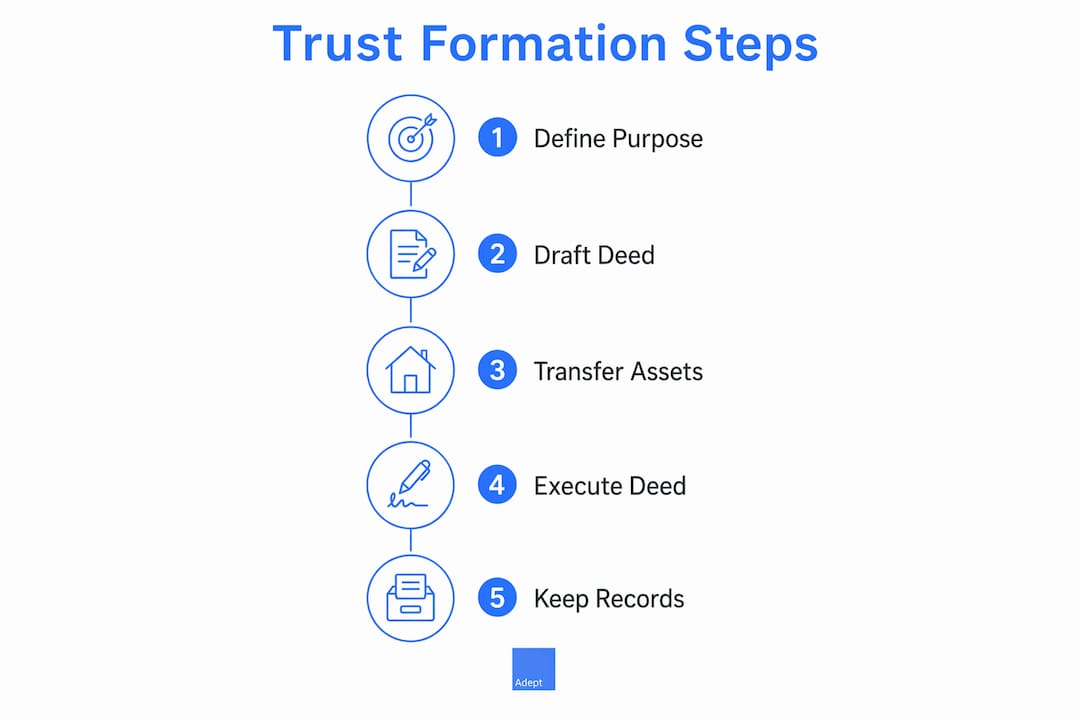

Step-by-step process to form and fund a trust in Singapore

Forming a trust in Singapore follows a defined sequence. Skipping or rushing any step creates constitutive defects that can invalidate the entire structure.

Step 1: Define the trust's purpose and structure. Before drafting any documents, identify the trust type. Common options include discretionary living trusts, fixed trusts, testamentary trusts, and charitable trusts. Each carries different drafting requirements and tax implications under IRAS guidelines.

Step 2: Draft the trust deed with legal assistance. The trust deed is the foundational document. It must specify the trust's purpose, identify the trustee and beneficiaries, define the trustee's powers and discretions, and address succession of trustees. Discretionary living trusts must be expressly manifested in writing complying with section 7 of the Civil Law Act, with beneficiaries and trust property clearly identified. A Letter of Wishes may accompany the deed to guide trustee discretion, but it is not legally binding.

Step 3: Transfer trust property to the trustee. This step is where many trusts fail. Trust property must be precisely identified and fully transferred to the trustee to avoid constitutive defects that render a trust void. True trust constitution hinges on actual legal transfer, not equitable intent. If the settlor fails to complete the transfer, ownership remains with the settlor and no trust exists in law.

The table below compares key considerations across the most common trust types:

| Trust type | Written deed required | Asset transfer method | Binding on trustee |

|---|---|---|---|

| Discretionary living trust | Yes, per Civil Law Act s.7 | Deed of transfer or assignment | Yes, subject to Letter of Wishes |

| Fixed trust | Yes | Legal title transfer | Yes, no discretion |

| Testamentary trust | Yes, via will | Probate and estate administration | Yes, upon death of settlor |

| Charitable trust | Yes | Transfer to charitable trustee | Yes, subject to Charities Act |

Step 4: Execute the deed and complete formalities. All parties must sign the trust deed before a witness. For immovable property, a separate conveyance deed in English is required. Retain certified copies of all executed documents.

Step 5: Maintain post-formation records. Trustees must keep accurate accounts of trust assets, income, and distributions. IRAS requires trustees to report trust income and file the relevant tax returns annually. Failure to maintain proper records is both a compliance breach and a breach of fiduciary duty.

Pro Tip: Engage a corporate services provider with trust administration experience to handle post-formation record-keeping. The administrative burden of trust compliance is frequently underestimated, and gaps in records are the most common trigger for regulatory scrutiny.

Regulatory compliance and ongoing obligations for trusts in Singapore

Singapore's regulatory framework for trusts is among the most structured in Asia. The Trust Companies Act 2005 restricts trust business to licensed companies or exempt persons, with MAS holding broad supervisory and enforcement powers. This framework applies to any entity carrying on trust business in Singapore, regardless of where the trust assets are located.

Key ongoing compliance obligations include:

- MAS licensing: Any entity providing trust services commercially must hold a valid MAS license or qualify for a statutory exemption. Exemptions are narrow and must be assessed carefully against the specific activities performed.

- AML/CFT compliance: Licensed Trust Companies must conduct customer due diligence, maintain transaction records, and file Suspicious Transaction Reports with the Suspicious Transaction Reporting Office (STRO) where required.

- Tax reporting to IRAS: Trustees are responsible for filing income tax returns on behalf of the trust. Singapore taxes trust income at the prevailing corporate rate of 17%, though specific exemptions may apply depending on the trust's structure and the residency of beneficiaries.

- Annual accounts and record-keeping: Trustees must maintain accurate financial records and prepare annual accounts. These records must be available for inspection by MAS and IRAS upon request.

- Trustee succession planning: The trust deed should include provisions for replacing trustees. Failure to address succession can result in the trust becoming unadministered if a sole trustee dies or becomes incapacitated.

Choosing a licensed trust company to act as trustee substantially reduces compliance risk. Licensed entities are subject to ongoing MAS supervision, which provides beneficiaries with a regulated point of accountability that individual trustees cannot offer.

Common mistakes and best practices in forming trusts in Singapore

The most frequent errors in Singapore trust formation are not procedural. They are substantive failures that strike at the legal validity of the trust itself.

- Failing the three certainties: Lacking these certainties invalidates beneficial interests regardless of formal documents. Courts will not save a trust where the settlor's intention is ambiguous or the beneficiary class is undefined.

- Incomplete asset transfer: Equitable intent does not substitute for legal transfer. If the settlor intends to place shares into trust but never executes a proper stock transfer form, the shares remain in the settlor's estate.

- Confusing a Letter of Wishes with a binding obligation: Letters of Wishes guide trustee discretion but carry no legal force. Settlors who treat them as binding instructions misunderstand the trust structure and may inadvertently undermine the trust's asset protection purpose.

- Neglecting trustee governance: Appointing a single individual trustee with no oversight mechanism creates governance risk. A co-trustee or protector provision provides checks on unilateral decisions.

- Failing to review the trust regularly: Tax laws, family circumstances, and regulatory requirements change. A trust deed drafted in 2015 may not reflect current IRAS guidance or MAS requirements.

"The most common error we see is not a drafting mistake. It is a client who believes the trust exists because the deed is signed, without ever completing the asset transfer. The deed is the intention. The transfer is the trust."

Reviewing directors' duties and responsibilities in the corporate context provides a useful parallel: just as directors carry personal liability for governance failures, trustees carry personal liability for trust administration failures. The standard is equally demanding.

For tax-efficient structuring, a tax-efficient investing checklist can help identify common trust setup errors and documentation gaps before they become enforcement issues.

Key takeaways

A valid Singapore trust requires the three certainties, complete asset transfer to the trustee, and ongoing regulatory compliance under MAS and IRAS frameworks.

| Point | Details |

|---|---|

| Three certainties are non-negotiable | Intention, subject matter, and objects must all be satisfied or the trust is void. |

| Asset transfer completes the trust | Signing the deed without transferring assets leaves ownership with the settlor. |

| Immovable property needs a separate deed | A signed trust deed alone is insufficient; a conveyance deed in English is legally required. |

| Trustee selection determines compliance risk | Licensed Trust Companies offer MAS-regulated accountability that individual trustees cannot match. |

| Ongoing obligations are substantial | Tax reporting to IRAS, AML/CFT compliance, and annual record-keeping are mandatory, not optional. |

What we have learned from Singapore trust formation in practice

From our experience advising clients on trust structures, the gap between understanding trust law in theory and executing it correctly in practice is wider than most people expect. Clients frequently arrive with a signed trust deed and no completed asset transfer. They believe the trust is operational. It is not.

The three certainties are taught in every law school, but certainty of subject matter causes the most real-world failures. Settlors describe assets in broad terms because they want flexibility. Courts interpret flexibility as uncertainty, and uncertainty voids the trust. Precision in drafting is not pedantry. It is the difference between a trust that holds and one that collapses under scrutiny.

On trustee selection, we consistently see clients underestimate the governance burden placed on individual trustees. A family member appointed as trustee out of convenience often lacks the compliance infrastructure to meet MAS expectations, particularly on AML/CFT obligations. A Licensed Trust Company costs more upfront, but the regulatory protection it provides is worth the premium, especially for trusts holding significant assets or operating across jurisdictions.

Protector provisions are underused. Settlors who want ongoing influence over trust decisions without retaining legal ownership should always consider appointing a protector with defined veto rights. This mechanism is well-recognized under Singapore law and provides a practical governance tool that does not compromise the trust's legal structure.

The regulatory environment is tightening. MAS has consistently raised compliance expectations for trust businesses over the past five years. Trusts formed without proper legal advice and licensed trustee oversight are increasingly exposed to enforcement action. Proactive governance is not optional. It is the baseline.

— Wandy & Terence

How Adept Corporate Services supports your trust formation

Adept Corporate Services works with individuals, families, and corporate clients navigating Singapore trust formation, from initial structure design through to ongoing compliance administration. Whether you need guidance on trust deed drafting, trustee selection, or MAS licensing requirements, our team provides direct, expert support without automated responses or generic templates.

For clients establishing corporate structures alongside trust arrangements, our company formation services cover the full spectrum of Singapore corporate law basics, including holding structure setup and shareholder agreement guidance. For a broader overview of how trust formation fits within Singapore's corporate services framework, the complete guide to corporate services provides detailed context on compliance, licensing, and entity selection. Contact Adept Corporate Services directly to speak with a real advisor about your trust structure.

FAQ

What is the three certainties rule in Singapore trust law?

The three certainties rule requires that a valid trust demonstrate certainty of intention, certainty of subject matter, and certainty of objects. Failing any one certainty invalidates the trust and leaves beneficial interests unenforceable.

Does a Singapore trust need to be registered?

Singapore does not maintain a public trust register for private express trusts, but trusts must comply with MAS licensing requirements if trust business is carried on commercially. Trustees must also register with IRAS for tax filing purposes.

What documents are required to form a trust in Singapore?

A trust deed is the primary document, and it must satisfy the three certainties and comply with the Civil Law Act. For immovable property, a separate conveyance deed in English is required under Civil Law Act 1909 section 7.

Can a foreign national be a trustee in Singapore?

Yes, foreign nationals may act as individual trustees in Singapore. However, any entity carrying on trust business commercially must hold a valid MAS license under the Trust Companies Act 2005, regardless of the trustee's nationality.

What is a protector in a Singapore trust?

A protector is an appointed individual or entity with defined powers to supervise the trustee, including veto rights over specified decisions. Protectors exercise oversight per the trust deed and provide a governance mechanism without holding legal title to trust assets.

Recommended

- Singapore Single Family Office 2026 Guide | Adept Corporate Services

- Starting and Setting Up a Business or Company in Singapore | Adept Corporate Services

- 2026 Statutory Compliance Calendar for a Singapore Company | Adept Corporate Services

- Why Singapore is the Best Place to Start a Company as a Foreigner in 2025 | Adept Corporate Services