A Singapore Special Purpose Vehicle (SPV) structure is a legally separate entity, most commonly a Private Company Limited by Shares (Pte. Ltd.), created to ring-fence a specific investment or business purpose under Singapore law. Understanding what is a Singapore SPV structure matters because it determines how you isolate financial risk, pool investor capital, and optimize tax treatment across international operations. The structure derives its legal force from Singapore's Companies Act, which grants separate legal personality and allows constitutional restrictions on permitted activities. For business professionals and investors, the SPV is not a special registration category. It is a purpose-built legal wrapper with defined governance, limited liability, and clear operational boundaries.

What is a singapore SPV structure under singapore law?

A Singapore SPV structure is defined by two Companies Act provisions working together. Section 19 grants separate legal personality, meaning the SPV is a distinct legal entity from its shareholders. Section 23 allows the company's constitution to restrict its activities to a single defined purpose, which is the core mechanism that makes an SPV function differently from a general operating company.

This distinction matters in practice. A general Pte. Ltd. can pivot, acquire unrelated assets, or take on new business lines. An SPV cannot, because its constitution prohibits it. That restriction is precisely what makes the structure credible to banks, counterparties, and co-investors. SPV status in Singapore derives from incorporation mechanics and constitutional restrictions, not from any dedicated SPV registry or special license.

The Accounting and Corporate Regulatory Authority (ACRA) registers all Singapore companies, including those used as SPVs. There is no separate ACRA category for SPVs. The legal effect comes entirely from how the company is structured, documented, and operated.

Which entity type should you use for a singapore SPV?

Singapore SPVs are typically Pte. Ltd. companies, but the Variable Capital Company (VCC) and Limited Partnership (LP) are also used depending on the investment strategy. Each entity type carries different legal, governance, and tax implications.

| Entity Type | Best For | Key Advantage | Key Trade-off |

|---|---|---|---|

| Private Limited (Pte. Ltd.) | Single-deal SPVs, startup equity | Familiar structure, bank-friendly | Contractual ring-fencing only |

| Variable Capital Company (VCC) | Fund managers, multi-portfolio | Statutory sub-fund segregation | Requires MAS-regulated manager |

| Limited Partnership (LP) | PE/VC funds, carried interest | Pass-through taxation, flexible GP/LP roles | No separate legal personality for LP itself |

The Pte. Ltd. remains the default choice for most deal-by-deal SPVs because it is straightforward to incorporate, widely recognized by banks and institutional counterparties, and governed by a well-established legal framework. The VCC framework, effective january 2020, introduced a more flexible corporate structure administered by ACRA and regulated by the Monetary Authority of Singapore (MAS). It allows fund managers to create multiple sub-funds under one umbrella entity, each with its own assets and liabilities.

The LP structure suits private equity and venture capital funds where general partners (GPs) manage the fund and limited partners (LPs) contribute capital without taking on management liability. Pass-through taxation is the primary draw for LP structures.

Pro Tip: If you are running a single co-investment deal, a Pte. Ltd. SPV is almost always the right starting point. Reserve the VCC for situations where you need to manage multiple portfolio companies under one regulated umbrella.

How does a singapore SPV operate in practice?

SPVs pool investor capital into a single vehicle to hold a target asset, such as startup equity or a convertible note, with investors participating through shares. This is the core operational model. The SPV holds the asset on behalf of all investors, and each investor's economic interest is proportional to their share class and ownership percentage.

A typical Singapore SPV has three categories of participants:

- Lead investor or deal sponsor: Manages the SPV, sources the deal, and holds a management share class with governance rights.

- Participating investors: Hold ordinary or preferred shares representing their economic stake in the underlying asset.

- Carry partners: Hold a separate share class entitling them to a percentage of profits above a defined return threshold, commonly 20%.

The constitution restricts the SPV to its defined purpose, such as holding shares in a specific target company. This restriction, combined with segregated bank accounts and clean accounting, creates the ring-fencing effect that protects each investor's exposure. Without these operational disciplines, the legal separation can be challenged by creditors or tax authorities.

Singapore SPVs are bank-friendly and counterparty-credible precisely because the governance structure is transparent. Share registers, constitutional documents, and financial statements are all maintained under the Companies Act, giving external parties a clear picture of the entity's purpose and ownership.

Pro Tip: Always open a dedicated bank account in the SPV's name before any capital is received. Commingling funds with a related entity, even temporarily, weakens the ring-fencing argument and creates accounting complexity that is difficult to unwind.

What are the tax implications of a singapore SPV?

Singapore does not impose a general capital gains tax, which is one of the primary reasons investors use Singapore SPVs for holding investments. The critical qualification is that gains are only tax-free if they are characterized as capital in nature rather than income from a trading activity. That distinction is not automatic.

The Singapore tax authority, the Inland Revenue Authority of Singapore (IRAS), looks at the facts and circumstances of each transaction to determine whether gains are capital or income. Key factors include the frequency of transactions, the holding period, the investor's stated intent at the time of acquisition, and the financing structure used.

The following practices support a capital gain characterization for SPV investments:

- Document investment intent at entry. Board resolutions and investment memos should state clearly that the SPV is acquiring the asset for long-term holding, not trading.

- Maintain consistent holding behavior. Frequent buying and selling of similar assets signals a trading pattern, which IRAS may treat as income-generating activity.

- Preserve transaction records. Evidence of investment intent and holding strategy supports capital treatment if IRAS reviews the SPV's tax position.

- Separate the SPV from operating entities. Mixing investment activity with operational revenue in the same entity blurs the characterization and increases tax risk.

Tax planning note: Singapore's lack of a general capital gains tax is a structural advantage, not a blanket exemption. SPVs must maintain clear documentation and consistent investment behavior to protect that advantage. Misunderstanding this distinction is one of the most common and costly errors investors make.

For VCC structures, the sub-fund segregation model adds a further layer of financial efficiency. Creditors of one sub-fund cannot claim against the assets of another sub-fund within the same VCC umbrella. This statutory protection goes beyond what a Pte. Ltd. SPV can achieve through contractual arrangements alone.

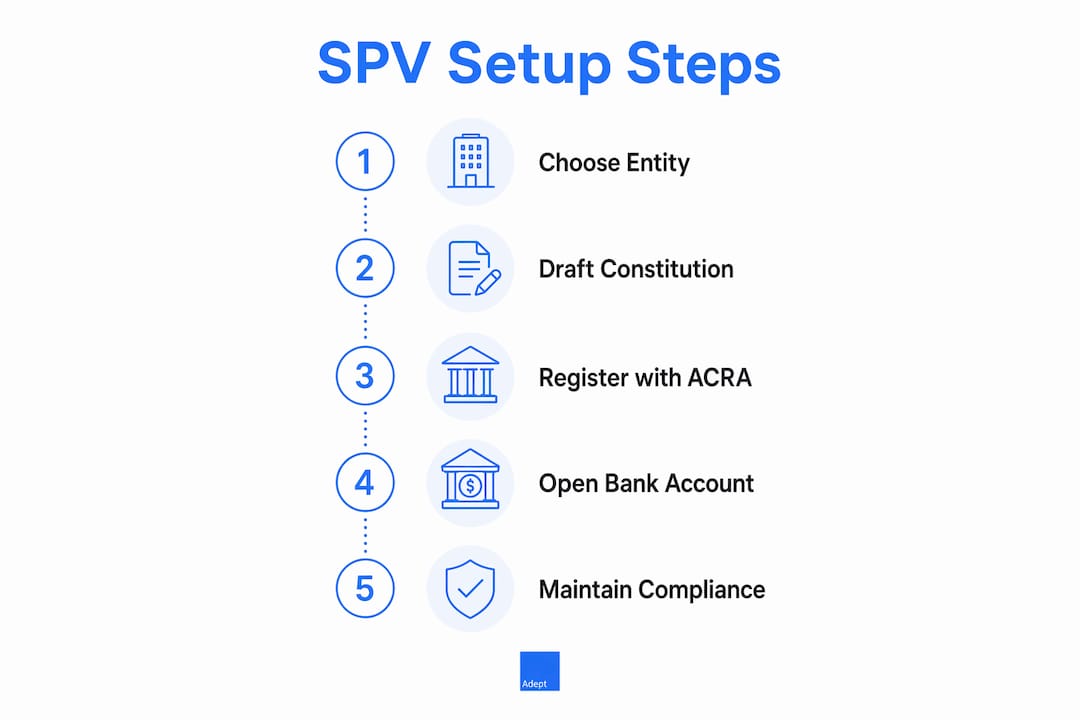

How to set up an SPV in singapore: practical steps

Setting up a Singapore SPV follows the standard company incorporation process under the Companies Act, with additional structuring steps specific to the SPV's purpose. The process is governed by ACRA and typically takes two to five business days for a straightforward Pte. Ltd. incorporation.

- Define the SPV's purpose. Before incorporation, document the specific investment or transaction the SPV will hold. This definition drives the constitutional restrictions and share class design.

- Draft the constitution. The constitution must include a restricted objects clause limiting the company's activities to the defined purpose. This is the legal foundation of the SPV structure.

- Incorporate with ACRA. File the incorporation documents, including the constitution, director and shareholder details, and registered address. ACRA registration is completed online through the BizFile+ portal.

- Issue shares and execute shareholder agreements. Allocate share classes to the lead investor, participating investors, and carry partners. Execute a shareholders' agreement governing governance rights, transfer restrictions, and exit mechanics.

- Open a dedicated bank account. The SPV must have its own bank account before receiving any investor capital. This is a non-negotiable compliance requirement for maintaining ring-fencing.

- Appoint a corporate secretary. Singapore law requires every company to appoint a qualified corporate secretary within six months of incorporation. The secretary maintains statutory registers and files annual returns with ACRA.

For foreign investors, additional considerations apply. Directors must include at least one Singapore-resident director, which is a statutory requirement under the Companies Act. Many foreign investors satisfy this through a corporate services provider that supplies a nominee director alongside secretarial and compliance support.

Ongoing compliance includes annual financial statements, corporate tax filings with IRAS, and annual returns to ACRA. SPVs holding investments in foreign entities may also have transfer pricing documentation requirements if related-party transactions are involved.

Pro Tip: Engage a corporate services provider before you begin drafting the constitution. The objects clause and share class structure must align precisely with your investment terms. Errors at this stage are expensive to correct after investors have signed subscription documents.

Key takeaways

A Singapore SPV structure derives its legal and financial power from constitutional purpose restrictions and operational discipline, not from any special registration category.

| Point | Details |

|---|---|

| Legal basis | Companies Act Sections 19 and 23 create separate legal personality and enable purpose restriction. |

| Entity selection | Pte. Ltd. suits single-deal SPVs; VCC suits fund managers needing statutory sub-fund segregation. |

| Tax efficiency | Singapore has no general capital gains tax, but gains must be characterized as capital through documented intent and consistent holding behavior. |

| Ring-fencing discipline | Segregated bank accounts and clean accounting are required to maintain the SPV's legal and financial isolation. |

| Setup process | ACRA incorporation takes two to five business days; a resident director and corporate secretary are statutory requirements. |

What we have learned from structuring singapore spvs

By Wandy & Terence

After working with dozens of investors setting up SPVs in Singapore, the most consistent mistake we see is treating the legal structure as the finish line. Investors incorporate the Pte. Ltd., draft a constitution, and assume the ring-fencing is complete. It is not. The ring-fencing is only as strong as the operational discipline behind it.

We have seen SPVs where the lead investor used the entity's bank account for unrelated expenses, or where accounting records mixed the SPV's investment income with the sponsor's management fees. In both cases, the legal separation became difficult to defend. The Companies Act gives you the tools. You have to use them correctly.

On entity selection, we advise clients to resist the temptation to use a VCC before they need one. The VCC framework is well-designed and the statutory sub-fund segregation is genuinely superior for complex portfolios. But it requires a MAS-regulated fund manager, which adds cost and regulatory overhead that most single-deal SPVs do not need. Start with a Pte. Ltd. and migrate to a VCC structure when your portfolio complexity justifies it.

The tax question deserves more caution than most investors apply. Singapore's absence of a general capital gains tax is real, but it is not unconditional. We have reviewed SPV structures where the transaction pattern, short holding periods, and lack of documented investment intent created a credible IRAS argument for income treatment. The investment holding tax treatment you expect is only available if you build the evidentiary record to support it from day one.

— Wandy & Terence

How adept corporate services supports your singapore SPV

Adept Corporate Services works with business professionals and investors at every stage of the SPV lifecycle, from initial structuring through ongoing compliance. Whether you are incorporating a Pte. Ltd. for a single co-investment or setting up a VCC for a multi-portfolio fund, the team at Adept Corporate Services provides direct, personal support with no automated responses.

Services include ACRA incorporation, constitution drafting, corporate secretarial compliance, fund administration and accounting, and MAS licensing advisory. Adept Corporate Services also assists with bank account opening for SPVs, including offshore entities, which is one of the most time-consuming steps for foreign investors. For a full overview of how Adept Corporate Services can support your Singapore company formation, contact the team directly for a consultation tailored to your investment structure.

FAQ

What is a singapore SPV structure?

A Singapore SPV is a legally separate entity, typically a Private Company Limited by Shares, incorporated under the Companies Act to hold a specific investment or asset. Its constitution restricts its activities to a defined purpose, creating legal and financial separation from its shareholders.

Does singapore tax SPV capital gains?

Singapore does not impose a general capital gains tax, but gains are taxable if characterized as income from a trading activity. SPVs must document investment intent and maintain consistent holding behavior to support capital treatment.

What is the difference between a pte. ltd. SPV and a VCC?

A Pte. Ltd. SPV uses contractual ring-fencing through its constitution and shareholder agreements, while a VCC provides statutory sub-fund segregation where creditors of one sub-fund cannot claim against another. The VCC requires a MAS-regulated fund manager.

How long does it take to set up an SPV in singapore?

ACRA incorporation for a Pte. Ltd. SPV typically takes two to five business days. Additional time is required for constitution drafting, share class structuring, and bank account opening, which can extend the total setup timeline to two to four weeks.

Do foreign investors need a local director for a singapore SPV?

Singapore law requires at least one Singapore-resident director for all locally incorporated companies, including SPVs. Foreign investors commonly satisfy this requirement through a corporate services provider that supplies a qualified nominee director.