Singapore GST registration is mandatory for any business whose taxable turnover exceeds S$1 million, and the Inland Revenue Authority of Singapore (IRAS) enforces this obligation under both retrospective and prospective assessment rules. Goods and Services Tax (GST) is a broad-based consumption tax levied at 9% on taxable supplies, and non-registered businesses cannot charge or reclaim it. For entrepreneurs setting up operations in Singapore, understanding the registration threshold, the online application process via the IRAS myTax Portal, and the new InvoiceNow e-invoicing obligations introduced in 2026 is not optional. This guide covers every stage of the GST registration process Singapore businesses face, from eligibility assessment through post-registration compliance.

Who needs to register for GST in Singapore?

GST registration requirements/gst-registration-deregistration/do-i-need-to-register-for-gst) in Singapore operate under two distinct views, and your obligation to register can be triggered by either one.

The retrospective view applies when your taxable turnover for the previous calendar year has exceeded S$1 million. Once that threshold is crossed, you must apply for GST registration within 30 days of the end of that calendar year. Missing this deadline exposes your business to backdated GST liabilities and financial penalties.

The prospective view applies when you have reasonable grounds to expect your taxable turnover to exceed S$1 million in the next 12 months. This is where many business owners are caught off guard. IRAS does not rely solely on past sales figures. Contracts, invoices, and accepted orders/gst-registration-deregistration/do-i-need-to-register-for-gst) are all valid evidence to substantiate a prospective registration, and you must register within 30 days of forming that reasonable expectation.

Beyond these two primary triggers, specific categories carry additional obligations:

- Overseas vendors supplying digital services to Singapore consumers must register under the Overseas Vendor Registration regime regardless of local turnover.

- Reverse charge applies to GST-registered businesses that procure services from overseas suppliers, requiring them to account for GST on those purchases.

- Voluntary registration is available to businesses below the S$1 million threshold, provided they meet IRAS's conditions and commit to remaining registered for at least two years.

Pro Tip: Monitor your taxable turnover on a rolling 12-month basis, not just at year-end. A single large contract win can push you over the threshold mid-year, triggering a prospective registration obligation immediately.

Voluntary registration is strategically valuable for businesses that incur significant GST on purchases. Registering allows you to claim input tax credits, improving cash flow. However, it also introduces compliance obligations, including quarterly GST return filing and record-keeping requirements that must be weighed carefully before applying.

What documents and prerequisites do you need before applying?

Preparation is the single factor that most directly determines whether your GST registration application is approved quickly or delayed. IRAS reviews applications using a risk-based approach/gst-registration-deregistration/applying-for-gst-registration) and may require a two-year guarantee from businesses it assesses as higher risk. Incomplete or inconsistent submissions are the primary cause of delays.

The core documents you need to prepare in soft copy before starting your application include:

- Business profile from the Accounting and Corporate Regulatory Authority (ACRA), confirming your registered business activities.

- Contracts, purchase orders, or invoices substantiating your taxable turnover, particularly for prospective registration.

- Financial statements or management accounts for the most recent period available.

- Bank account details for GIRO setup, which IRAS uses to process GST payments and refunds.

For voluntary registrants, two additional prerequisites are non-negotiable. First, all directors and preparers involved in the GST registration must complete the IRAS GST e-Learning course/gst-registration-deregistration/applying-for-gst-registration) before submitting the application. Second, a GIRO application or eGIRO setup must be submitted alongside or prior to the GST registration form. Skipping either step results in an incomplete application that IRAS will not process.

Pro Tip: Create a document checklist and assemble all soft copies before you log into the myTax Portal. Starting the GST registration form/gst-registration-deregistration/guide-to-completing-gst-registration-form) without your documents ready is one of the most common practical pitfalls, as the draft window is only 14 days.

Good record-keeping practices are also a prerequisite in a broader sense. IRAS expects businesses to maintain five years of records post-registration, so establishing organized filing systems before you register sets the right foundation for ongoing compliance.

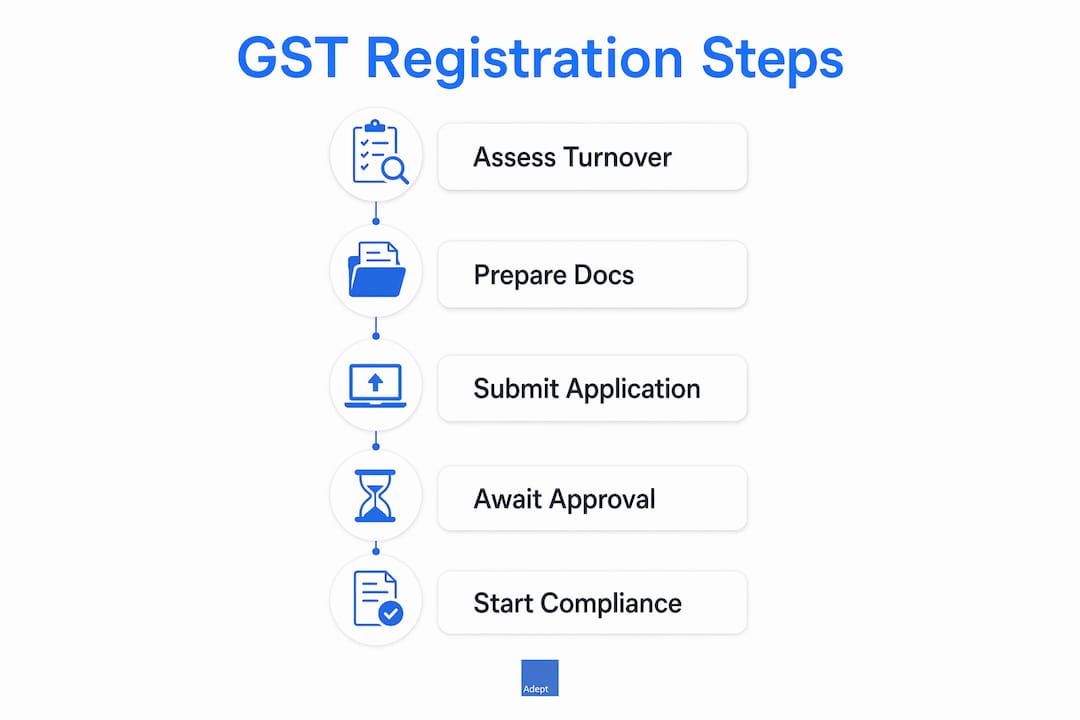

How to register for GST online via IRAS myTax Portal

The GST F1 application form/gst-registration-deregistration/guide-to-completing-gst-registration-form) is submitted entirely online through the IRAS myTax Portal. The process follows a structured sequence, and understanding each stage prevents errors that delay approval.

- Log in to myTax Portal using your Singpass credentials. Select the correct taxpayer category, whether you are registering as a sole proprietor, partnership, or company, as this determines which fields appear in the form.

- Access the "Register for GST" digital service from the GST menu. This launches the GST F1 form, which is divided into distinct sections covering your business profile, principal activities, and taxable supply details.

- Complete the business activity section accurately. IRAS cross-references your declared activities against your ACRA business profile. Discrepancies between the two are a common reason for follow-up queries.

- Declare your taxable supplies and accounting period. You will need to specify whether you are registering under the retrospective or prospective view and provide the supporting turnover figures. You also select your preferred GST accounting period, typically quarterly.

- Complete the InvoiceNow compliance section. From 1 April 2026 onward, new voluntary registrants must confirm their readiness to submit invoice data via InvoiceNow. This is a mandatory declaration, not an optional field.

- Upload supporting documents within the 14-day draft window. Once submitted, IRAS will review your application and notify you of the effective GST registration date.

| Application stage | Typical timeframe |

|---|---|

| Document preparation | 3 to 7 days |

| Form completion and submission | 1 to 2 days |

| IRAS review and approval | 10 to 14 business days |

| Effective GST registration date | Backdated to obligation date or approval date |

Pro Tip: Double-check that your declared business activities match your ACRA profile exactly before submitting. A mismatch between the two is one of the most frequent causes of IRAS follow-up queries and delays.

The effective GST registration date matters significantly. For compulsory registrants, it is typically backdated to the date the obligation arose, meaning you may need to account for GST on supplies made before your approval was confirmed. For voluntary registrants, the effective date is generally the date IRAS approves the application.

What are your GST compliance obligations after registration?

Registration is the beginning of an ongoing compliance relationship with IRAS, not a one-time administrative task. From your effective GST registration date, you are legally required to charge GST at 9% on all taxable supplies and issue tax invoices to your customers. Failure to charge GST from the correct date creates a liability that falls on your business, not your customers.

Your core post-registration obligations include:

- Filing GST returns (Form GST F5) on a quarterly basis, declaring output tax collected and input tax claimable.

- Maintaining records for a minimum of five years, including tax invoices, receipts, import permits, and contracts.

- Notifying IRAS of any changes to your business activities, accounting periods, or contact details within 30 days.

- Complying with InvoiceNow requirements as they phase in across your business category.

The InvoiceNow obligation deserves particular attention in 2026. IRAS and the Infocomm Media Development Authority (IMDA) are rolling out a phased InvoiceNow mandate for GST-registered businesses between 2025 and 2031. New voluntary GST registrants from 1 April 2026 must transmit invoice data to IRAS via InvoiceNow-accredited access points. Compulsory registrants will be brought into scope in subsequent phases.

| Business category | InvoiceNow obligation start date |

|---|---|

| New voluntary registrants | 1 April 2026 |

| New compulsory registrants | To be confirmed in later phases |

| Existing GST-registered businesses | Phased rollout through 2031 |

Aligning your accounting systems with InvoiceNow early reduces compliance risk as the mandate expands. Accounting software such as Xero, QuickBooks, and MYOB have InvoiceNow-ready integrations available in Singapore, and selecting a compliant solution before you register avoids a costly system migration later. The 2026 statutory compliance calendar published by Adept Corporate Services provides a useful reference for tracking all GST and invoicing deadlines throughout the year.

Key takeaways

Successful GST registration in Singapore requires accurate turnover monitoring, complete document preparation, precise form completion via myTax Portal, and proactive InvoiceNow system readiness from day one.

| Point | Details |

|---|---|

| Registration threshold | Businesses exceeding S$1 million in taxable turnover must register within 30 days under retrospective or prospective rules. |

| Voluntary registration prerequisites | Directors and preparers must complete the IRAS GST e-Learning course and submit a GIRO application before applying. |

| Application window | Supporting documents must be uploaded within 14 days of starting the GST F1 form on myTax Portal. |

| InvoiceNow obligation | New voluntary registrants from 1 April 2026 must transmit invoice data via InvoiceNow-accredited access points. |

| Post-registration compliance | GST-registered businesses must file quarterly returns, maintain five years of records, and charge 9% GST from the effective date. |

What we have learned from guiding businesses through GST registration

The most consistent mistake we see is businesses treating GST registration as a reactive task. A company crosses the S$1 million threshold, realizes it should have registered months earlier, and then faces backdated liabilities and a rushed application process. The prospective registration rule exists precisely to prevent this, but it only works if you are actively forecasting your pipeline, not just reviewing last year's accounts.

Voluntary registration is frequently underutilized by early-stage businesses. If you are incurring significant GST on purchases, such as office leases, professional services, or equipment, registering voluntarily can generate meaningful input tax recoveries. The two-year commitment requirement is a real constraint, but for most businesses with genuine commercial activity, it is not a deterrent.

The InvoiceNow requirement is the area where we are seeing the most unpreparedness in 2026. Many business owners assume it is a distant obligation. For new voluntary registrants, it is not. It is a day-one requirement from 1 April 2026, and integrating with an accredited access point takes time. Selecting InvoiceNow-ready tax compliance software before you register is the most practical way to avoid a compliance gap at the point of registration.

Our broader advice: treat GST registration as a structured project with defined milestones, not an administrative form to fill out. Prepare your documents, complete the e-Learning course, confirm your InvoiceNow readiness, and then submit. That sequence, done in order, produces approvals without delays.

— Wandy & Terence

How Adept Corporate Services supports your GST registration

Adept Corporate Services provides end-to-end support for Singapore businesses navigating GST registration and ongoing compliance. From assessing your registration obligation and preparing the required supporting documents to completing the GST F1 application on the IRAS myTax Portal, the Adept team manages the process with precision. Adept also advises on InvoiceNow readiness, helping you select and integrate accredited accounting solutions before your registration takes effect. For businesses setting up operations in Singapore, Adept's corporate treasury and business setup services cover GST registration as part of a broader compliance framework. Speak directly with a qualified advisor, no chatbots, no automated responses, just expert guidance from people who know Singapore tax compliance in depth.

FAQ

What is the GST registration threshold in Singapore?

Businesses must register for GST/gst-registration-deregistration/do-i-need-to-register-for-gst) when their taxable turnover exceeds S$1 million in the previous calendar year or when they reasonably expect to exceed that amount in the next 12 months. Registration must be submitted within 30 days of the obligation arising.

Can a business register for GST voluntarily below the threshold?

Yes. Businesses with taxable turnover below S$1 million may apply for voluntary GST registration, provided they complete the IRAS GST e-Learning course, submit a GIRO application, and commit to remaining registered for at least two years.

How long does IRAS take to approve a GST registration application?

IRAS typically processes GST registration applications within 10 to 14 business days, provided all supporting documents are complete and accurate. Incomplete submissions or risk-based reviews can extend this timeline.

What is the InvoiceNow requirement for GST-registered businesses?

InvoiceNow is a phased mandate requiring GST-registered businesses to transmit invoice data to IRAS via accredited access points. New voluntary registrants from 1 April 2026 are the first group subject to this obligation, with compulsory registrants and existing businesses brought in during subsequent phases through 2031.

What happens if a business registers for GST late?

Late registration exposes the business to backdated GST liabilities from the date the obligation arose, meaning the business must account for GST on supplies made during the unregistered period. IRAS may also impose financial penalties for non-compliance.