Singapore's flat 17% corporate tax rate makes the country sound like a simple place to handle business taxes. It isn't. Singapore corporate income tax filing involves multiple forms, strict deadlines, Corppass authorization requirements, and eligibility rules that trip up even experienced finance teams. Get it wrong and you face fines, IRAS inquiries, and missed rebates worth thousands of dollars. This guide covers everything you need to file correctly for Year of Assessment 2026, from choosing the right form to claiming the rebates your company has already earned.

Table of Contents

- Key Takeaways

- Understanding Singapore corporate income tax filing requirements

- How the Singapore corporate tax filing process works in 2026

- Choosing the right filing form

- 2026 CIT rebates and cash grants

- Common pitfalls and how to avoid them

- My take on what businesses consistently get wrong

- How Adept-cs can handle your corporate tax filing

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Two-step filing process | Submit ECI within 3 months of your financial year end, then file the annual return by November 30. |

| Form selection matters | Choosing the wrong filing form triggers IRAS inquiries and additional compliance work. |

| 2026 rebate opportunity | A 40% CIT rebate plus a minimum S$1,500 cash grant is available for companies with local CPF contributions. |

| Corppass access is critical | Set up Corppass "Approver" authorization before your deadline, not the week before filing. |

| Dormant does not mean exempt | Companies without business activity must still file unless IRAS explicitly grants a waiver. |

Understanding Singapore corporate income tax filing requirements

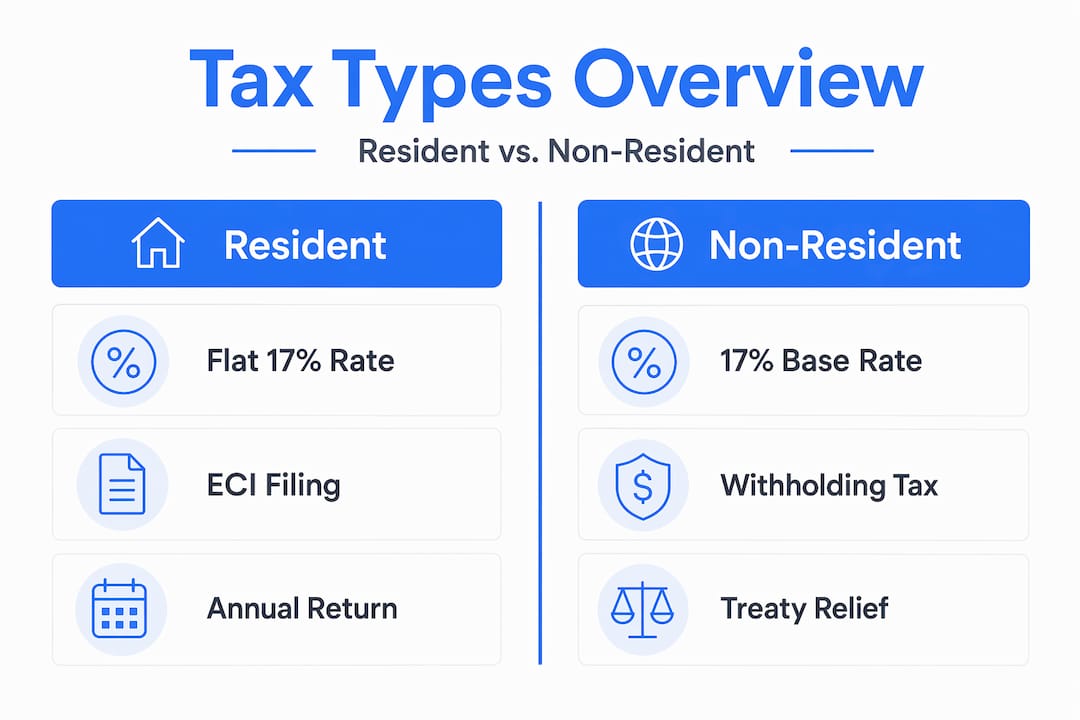

Before you can file correctly, you need to understand what you are actually filing on. Singapore taxes both resident and non-resident companies on income that is accrued or received in Singapore. That distinction matters more than most business owners realize.

Capital gains are generally excluded from taxable income, which is one of the genuine Singapore corporate tax advantages explained repeatedly in investment guides. What those guides often skip is the nuance: if your company regularly buys and sells assets as a business activity, IRAS may treat those gains as trading income, not capital gains.

The 17% flat rate applies to chargeable income, which is your gross income minus allowable deductions, capital allowances, and reliefs. Here is what that means in practice:

- Business expenses directly incurred in producing income are deductible.

- Capital allowances let you write down the cost of qualifying plant and machinery over time.

- Losses can be carried forward indefinitely or, under certain conditions, carried back one year.

- Start-up tax exemption gives new companies a 75% exemption on the first S$100,000 of chargeable income and a 50% exemption on the next S$100,000 for their first three years of assessment.

Non-resident companies face an additional layer: withholding tax applies to certain Singapore-sourced payments like royalties, interest, and service fees paid to them. If you operate through a Singapore subsidiary rather than a branch, the tax treatment differs in ways that affect your holding structure planning.

Pro Tip: If your company has foreign-sourced income, check whether Singapore has a tax treaty with that country. Treaty provisions can reduce or eliminate double taxation on dividends, royalties, and interest, which directly affects your chargeable income calculation.

How the Singapore corporate tax filing process works in 2026

The Singapore corporate tax filing process runs in two stages, and missing either one creates problems.

Stage 1: Estimated Chargeable Income (ECI)

ECI is your company's estimate of taxable income for the financial year, filed before your full accounts are finalized. The two-step filing system allows IRAS to compute provisional taxes early and reconcile them against your final return later. You file ECI through the myTax Portal within three months of your financial year end. So if your financial year ends December 31, 2025, your ECI is due by March 31, 2026.

Companies with annual revenue below S$5 million and a nil ECI may qualify for an ECI filing waiver, but you must verify this. Do not assume the waiver applies.

Stage 2: Annual Corporate Income Tax Return

The annual return deadline for Year of Assessment 2026 is November 30, 2026. This applies to all companies, including those with no income, those operating at a loss, and dormant companies unless IRAS has explicitly granted a waiver.

Here is the step-by-step process for filing your annual return:

- Confirm your Corppass authorization. Your company's Corppass Administrator must assign you the "Approver" role for Corporate Tax before you can submit anything on myTax Portal.

- Prepare your tax computation. Reconcile your financial statements with your tax position, identifying all allowable deductions, capital allowances, and exemptions.

- Select the correct filing form (covered in detail in the next section).

- Log in to myTax Portal using your Corppass credentials and complete the return.

- Review and submit. Once submitted, you can track your filing status and any IRAS correspondence through the same portal.

- Check for waiver status if you believe your company qualifies. Use the "Update Corporate Profile" digital service on myTax Portal to verify, not to assume.

Corppass "Approver" authorization is a prerequisite for submission, and delays in setting it up are one of the most common reasons companies miss deadlines despite having all their financial data ready. Set this up at the start of your financial year, not in November.

Pro Tip: Use the IRAS digital notification service to receive filing reminders. It sounds basic, but many companies with lean finance teams miss deadlines simply because no one tracked the calendar. Pair this with Adept-cs's 2026 compliance calendar to map every deadline across your full statutory obligations.

Choosing the right filing form

Selecting the appropriate form is often where companies make avoidable errors. IRAS offers four distinct options, and using the wrong one creates additional compliance workload and can trigger inquiries.

| Form | Who it's for | What's required |

|---|---|---|

| Form C | Companies with complex tax positions, significant revenue, or those not eligible for simplified forms | Full financial statements, detailed tax computations, supporting schedules |

| Form C-S | Companies with annual revenue up to S$5 million, taxable income only from Singapore, and no specific tax treatments | Simplified return with fewer fields |

| Form C-S (Lite) | Companies with annual revenue of S$200,000 or less | Only six essential fields required |

| Dormant Company | Companies with no business activities and no income | Minimal disclosure, subject to IRAS waiver eligibility |

Form C-S (Lite) is the most streamlined option available, but it is not suitable for companies with complex tax positions, carry-forward losses, or capital allowance claims. Using it when you do not qualify is not a shortcut. It is a compliance risk.

A few things to verify before choosing your form:

- Does your company claim group relief, investment allowances, or specific tax incentives? If yes, Form C is likely required.

- Is your revenue genuinely below the threshold, or are you excluding certain income streams that IRAS would include?

- If you have foreign-sourced income or are part of a holding structure, simplified forms may not capture your full tax position accurately.

You can review eligibility criteria in detail through Adept-cs's Form C-S and Form C guide before making your selection.

2026 CIT rebates and cash grants

The 2026 filing year comes with meaningful relief for companies that qualify. For Year of Assessment 2026, companies receive a 40% rebate on corporate tax payable, capped at S$30,000. Companies that employed at least one local employee with CPF contributions in 2025 also receive a minimum S$1,500 CIT Rebate Cash Grant, even if their tax payable is zero.

Here is what that looks like in practice. A company with S$200,000 in chargeable income owes S$34,000 in tax at 17%. After the 40% rebate, that drops to S$20,400. If the company qualifies for the cash grant, the effective tax burden falls further. IRAS applies these rebates automatically after you file. You do not need to claim them separately.

The types of Singapore corporate tax exemptions available go beyond rebates. Start-up exemptions, partial exemptions for established companies, and sector-specific incentives all reduce the effective rate below 17% for many businesses. The key is that you must file accurately to receive what you are entitled to. Errors in your ECI or annual return can delay or reduce your rebate application.

Pro Tip: If your company had no local employees with CPF contributions in 2025, you still qualify for the 40% rebate on tax payable, but you miss the S$1,500 cash grant. For holding companies or companies with only foreign employees, this distinction affects your cash flow planning for 2026.

Common pitfalls and how to avoid them

Most compliance failures in Singapore corporate income tax filing come down to a handful of recurring issues, not complex tax law.

- Corppass delays. Operational failures typically relate to Corppass authorization problems rather than missing financial data. Assign the "Approver" role early and verify access well before the November deadline.

- Assuming dormant status waives filing. It does not. Waivers must be verified through the "Update Corporate Profile" service on myTax Portal. A company that assumes it is exempt and files nothing faces late filing penalties.

- Accounting-tax mismatches. IRAS scrutinizes the nature and origin of income to confirm taxability. If your financial statements and tax computation tell different stories, expect follow-up questions. Effective reconciliation between the two is not optional.

- Inadequate recordkeeping. Singapore requires companies to retain records for at least five years. Poor documentation makes it impossible to substantiate deductions or capital allowances if IRAS queries your return. Adept-cs's guide on Singapore recordkeeping requirements covers what you need to keep and how to organize it.

- Late filing penalties. Fines for late submission can reach S$5,000, and IRAS can issue a summons for non-compliance. The penalty is not proportional to your tax liability. A dormant company with zero income faces the same fine as an active one.

Pro Tip: Build a pre-filing checklist that covers Corppass access, waiver status, form eligibility, and accounting-tax reconciliation. Run through it 60 days before your deadline. That buffer gives you time to fix problems without rushing.

My take on what businesses consistently get wrong

I have worked with enough Singapore-based businesses to say this plainly: the flat 17% rate creates a false sense of simplicity. Companies assume that because the rate is straightforward, the filing must be too. That assumption costs them.

What I see most often is not fraud or aggressive tax planning gone wrong. It is operational unpreparedness. A company's accountant has the numbers ready in October, but nobody set up Corppass authorization for the new finance director who joined in August. The deadline passes. The fine arrives.

The second most common issue is form selection. I have seen companies file Form C-S when their tax position clearly required Form C, simply because C-S looked easier. The simplified forms are genuinely useful for qualifying companies, but using them incorrectly signals to IRAS that you have not reviewed your position carefully. That draws attention you do not want.

My honest advice: treat the filing calendar as a year-round process, not a November sprint. Set up your digital access in January. Reconcile your accounts quarterly. Verify your form eligibility before your financial year closes, not after. Companies that approach it this way rarely face penalties and consistently capture the rebates and exemptions they are entitled to.

— Terence

How Adept-cs can handle your corporate tax filing

Staying compliant with Singapore's corporate income tax requirements takes more than knowing the rules. It takes consistent execution across deadlines, forms, reconciliations, and digital systems throughout the year.

Adept Corporate Services works directly with businesses across Singapore to manage the full corporate tax compliance cycle, from ECI preparation and form selection to annual return submission and IRAS correspondence. Our team handles Corppass authorization, accounting-tax reconciliation, and rebate optimization so nothing falls through the cracks. We also offer tax advisory services for businesses with more complex structures, including holding companies and companies with foreign-sourced income. No chatbots, no automated replies. Just experienced professionals who know your file. Reach out to Adept-cs to make your 2026 filing straightforward.

FAQ

What is the corporate tax filing deadline for 2026?

All companies must file their Year of Assessment 2026 Corporate Income Tax Return by November 30, 2026. This applies even to companies with no income or those operating at a loss, unless IRAS has granted a specific waiver.

What is the difference between ECI and the annual tax return?

ECI is an estimate of your chargeable income filed within three months of your financial year end. The annual return is the final, complete filing submitted by November 30 each year. Both are mandatory steps in the Singapore corporate tax filing process.

Can a dormant company skip filing?

No. Dormant companies must still file unless IRAS explicitly grants a waiver. You must verify your waiver status using the "Update Corporate Profile" service on myTax Portal. Assuming exemption without confirmation is a compliance risk.

Who qualifies for Form C-S (Lite)?

Companies with annual revenue of S$200,000 or less qualify for Form C-S (Lite), which requires only six essential fields. Companies with complex tax positions, capital allowance claims, or carry-forward losses should use Form C regardless of revenue size.

How does the 2026 CIT rebate work?

IRAS automatically applies a 40% rebate on corporate tax payable for Year of Assessment 2026, capped at S$30,000. Companies that employed at least one local employee with CPF contributions in 2025 also receive a minimum S$1,500 cash grant, even if their tax payable is nil.

Recommended

- Singapore Single Family Office 2026 Guide | Adept Corporate Services

- 2026 Statutory Compliance Calendar for a Singapore Company | Adept Corporate Services

- Professional Tax Advisory Services in Singapore | Adept Corporate Services

- Singapore Record Keeping Requirements: A Practical Guide to Tax Compliance for Small Businesses | Adept Corporate Services