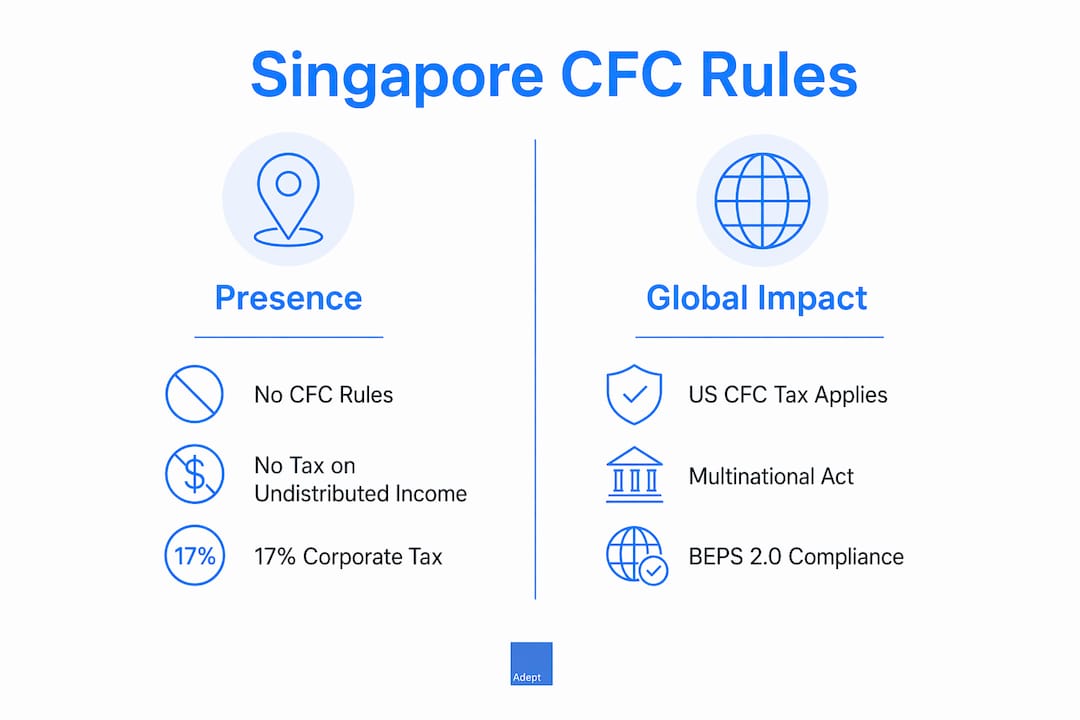

Singapore does not have controlled foreign corporation (CFC) rules, which sets its tax regime apart from the United States, the United Kingdom, Germany, and most other major economies. This absence is not an oversight. It reflects a deliberate policy choice rooted in Singapore's territorial tax system, its flat 17% corporate income tax rate, and its position as a hub for international business. For North American business owners and corporate managers with Singapore subsidiaries or holding structures, understanding what this means in practice is critical. Singapore's lack of CFC rules does not mean a compliance-free environment. The Inland Revenue Authority of Singapore (IRAS) enforces strict filing obligations, and the Multinational Enterprise (Minimum Tax) Act 2024 now introduces a 15% global minimum tax for large multinationals.

What are singapore controlled foreign corporation rules?

Controlled Foreign Corporation rules, commonly called CFC rules, are anti-avoidance provisions that allow a country to tax its residents on income earned by foreign subsidiaries they control. The core purpose is to prevent profit shifting. Without CFC rules, a company based in a high-tax country could park passive income in a low-tax foreign subsidiary and defer or avoid home-country taxation indefinitely.

The United States applies CFC rules under Subpart F of the Internal Revenue Code, targeting passive income, related-party sales income, and certain foreign base company income earned by controlled foreign corporations. The United Kingdom applies its own CFC regime under the Taxation (International and Other Provisions) Act 2010. Germany, France, Japan, and Australia all maintain comparable frameworks.

CFC rules typically operate through three mechanisms:

- Ownership threshold: The parent company must own a controlling stake, often 50% or more, in the foreign entity.

- Income type: Only certain categories of income, usually passive income like dividends, interest, and royalties, trigger CFC attribution.

- Tax differential: The foreign subsidiary must be subject to a tax rate significantly below the home country's rate to trigger the rules.

The practical effect is that a U.S. parent company with a Singapore subsidiary may still face U.S. CFC tax implications on certain income earned by that subsidiary, regardless of Singapore's own rules. North American business owners must account for their home-country CFC obligations even when operating through Singapore.

Does singapore have CFC rules?

Singapore does not impose CFC rules, meaning undistributed income sitting in a foreign subsidiary is generally not taxed at the Singapore parent level. This is a direct consequence of Singapore's territorial tax system. Singapore taxes income on a source basis: income arising in Singapore is taxable, and foreign-sourced income is generally exempt unless remitted under specific conditions.

This policy creates genuine advantages for multinational structures. A Singapore holding company that owns subsidiaries in Vietnam, Indonesia, or the Philippines does not face a Singapore-level tax charge on profits those subsidiaries retain. The income is taxed only in the jurisdiction where it arises, and Singapore does not reach across borders to impose additional tax on undistributed earnings.

Singapore's 17% flat corporate tax rate and extensive network of tax treaties with over 90 countries reinforce this attractiveness. The Economic Development Board (EDB) and IRAS also administer sector-specific incentive programs that can reduce effective tax rates further for qualifying activities.

The landscape is shifting for large multinationals, however. Singapore enacted the Multinational Enterprise (Minimum Tax) Act 2024 to align with the OECD's BEPS 2.0 framework, introducing a 15% global minimum tax for in-scope MNEs starting fiscal year 2025. This does not replicate traditional CFC rules, but it does impose a floor on effective tax rates across group entities. The compliance focus shifts from attribution of subsidiary income to ensuring no group entity falls below the 15% threshold.

Pro Tip: If your group's consolidated revenue exceeds EUR 750 million (approximately USD 810 million), your Singapore entity is likely in scope for the Multinational Enterprise (Minimum Tax) Act. Confirm your exposure with a qualified Singapore tax advisor before fiscal year 2025 filings close.

Singapore corporate tax filing requirements for foreign companies

Tax residency in Singapore is determined by where key management and control decisions are made, not by where a company is incorporated or where its bank accounts are held. A company incorporated in Delaware but managed from Singapore is treated as a Singapore tax resident. That status triggers full Singapore corporate income tax filing obligations and grants access to Singapore's double tax treaty network.

Foreign companies with Singapore-sourced income or with management and control exercised in Singapore must file corporate income tax with IRAS. Mere incorporation or the existence of a Singapore bank account alone does not create a filing obligation. Income generation or a permanent establishment presence is the trigger.

Key filing and compliance requirements include:

- Annual tax return (Form C, Form C-S, or Form C-S Lite): Filed with IRAS by November 30 each year for the preceding financial year.

- Estimated Chargeable Income (ECI): Filed within three months of the financial year end.

- Audited financial statements: Required for companies that exceed two of three thresholds: SGD 10 million in revenue, SGD 10 million in assets, or 50 employees. Companies below these thresholds may qualify for audit exemption.

- Registered office: Must be maintained in Singapore and accessible for at least five hours during business days under the Companies Act 1967.

- Annual General Meeting and annual return: Filed with the Accounting and Corporate Regulatory Authority (ACRA).

The entity structure you choose also determines your tax treatment. Foreign companies operating through a Singapore subsidiary are treated as separate legal entities and can access startup tax exemptions. Startup exemptions apply only to qualifying Singapore-incorporated companies and are not available to foreign company branches. A branch is treated as an extension of the foreign parent, which limits both exemptions and treaty access.

Failure to file can result in estimated assessments by IRAS, which typically produce higher tax liabilities than accurate self-reported figures. IRAS monitors cross-border operations closely, and late filings attract penalties that compound over time.

How BEPS 2.0 affects multinationals with singapore operations

BEPS 2.0 Pillar Two is the OECD's framework for a global minimum corporate tax. Singapore's Multinational Enterprise (Minimum Tax) Act 2024 implements Pillar Two for fiscal years starting on or after january 1, 2025. This is the most significant change to business taxation in Singapore in a generation.

The Act introduces two primary mechanisms:

- Income Inclusion Rule (IIR): A Singapore parent company must top up tax on low-taxed income earned by its foreign subsidiaries if those subsidiaries pay an effective tax rate below 15%.

- Domestic Top-up Tax (DTT): Singapore applies a top-up tax domestically to ensure Singapore entities within an in-scope group meet the 15% minimum, preserving Singapore's right to collect revenue before other jurisdictions can apply their own top-up rules.

The difference between this framework and traditional CFC rules is structural. CFC rules attribute subsidiary income to the parent and tax it at the parent's domestic rate. BEPS 2.0 does not attribute income. It simply imposes a floor. If a subsidiary pays 12% effective tax in a third country, the parent jurisdiction collects the 3% difference. The income stays in the subsidiary. Only the tax gap is addressed.

For corporate managers, the compliance steps are concrete:

- Determine whether your group's consolidated revenue exceeds EUR 750 million in at least two of the four preceding fiscal years.

- Map the effective tax rates of every group entity across all jurisdictions.

- Identify entities where the effective rate falls below 15% and quantify the top-up exposure.

- Engage a Singapore tax advisor to assess IIR and DTT obligations before the first affected filing period.

- Review existing incentive arrangements with IRAS or EDB to understand how they interact with the minimum tax calculation.

Pro Tip: Singapore's DTT is designed to protect Singapore's tax base. If your Singapore entity benefits from a reduced effective rate through EDB incentives, the DTT may recapture some of that benefit. Review incentive agreements carefully before assuming they survive BEPS 2.0 intact.

How to register and maintain compliance as a foreign company

Foreign companies establishing a place of business in Singapore must register with ACRA under the Companies Act 1967. The registration options include representative offices, branches, subsidiaries, and variable capital companies, each carrying different tax and legal consequences. Subsidiaries are the most common choice for North American businesses because they offer limited liability, full treaty access, and eligibility for startup tax exemptions.

The compliance calendar for a Singapore company is structured and non-negotiable. Missing deadlines with ACRA or IRAS triggers penalties, and repeated non-compliance can result in striking off the company register. For a detailed view of all statutory deadlines, the 2026 compliance calendar published by Adept Corporate Services provides a practical reference.

The table below compares the three most common foreign business structures in Singapore:

| Structure | Tax Treatment | Liability | Startup Exemption |

|---|---|---|---|

| Subsidiary | Separate Singapore tax resident entity | Limited to subsidiary | Available if qualifying conditions met |

| Branch | Extension of foreign parent | Parent bears liability | Not available |

| Representative Office | No commercial activity permitted | N/A | Not applicable |

Proper structural planning at the outset is far less costly than reorganizing after operations begin. Changing from a branch to a subsidiary after the fact requires new registration, asset transfers, and potential tax consequences in both Singapore and the home jurisdiction.

Engaging a corporate service provider for registration and ongoing compliance is not optional for most foreign companies. ACRA requires a locally resident director, a registered office address, and a company secretary. These requirements cannot be met remotely from North America without local support.

Key takeaways

Singapore's absence of CFC rules is a structural advantage, but BEPS 2.0 and Singapore's own filing requirements mean that compliance obligations remain substantial for foreign companies and large multinationals.

| Point | Details |

|---|---|

| No CFC rules in Singapore | Undistributed foreign subsidiary income is not taxed at the Singapore parent level. |

| BEPS 2.0 applies from 2025 | MNEs with EUR 750 million+ revenue face a 15% global minimum tax under the Multinational Enterprise (Minimum Tax) Act. |

| Tax residency is management-based | Singapore taxes companies where management and control are exercised, not where they are incorporated. |

| Entity structure determines tax access | Subsidiaries access startup exemptions and tax treaties; branches do not. |

| Non-compliance carries real penalties | IRAS issues estimated assessments and penalties for late or missing filings. |

Singapore's tax regime rewards the prepared

From our experience working with North American businesses entering Singapore, the most common mistake is treating the absence of CFC rules as a signal that Singapore tax compliance is simple. It is not simple. It is structured, predictable, and manageable, but only if you approach it correctly from day one.

The territorial system and the 17% flat rate are genuine advantages. We have seen clients build efficient holding structures in Singapore that materially reduce their global effective tax rates within the bounds of the law. Those outcomes are achievable. They require proper entity selection, accurate residency analysis, and disciplined filing from the start.

BEPS 2.0 has raised the stakes for larger groups. The Multinational Enterprise (Minimum Tax) Act 2024 is not theoretical. It applies to fiscal years starting in 2025, and the compliance infrastructure required, including country-by-country reporting, effective tax rate calculations, and top-up tax filings, demands preparation well in advance. Groups that wait until the filing deadline to assess their exposure will face compressed timelines and elevated risk.

Our consistent advice to clients is this: invest in the right structure before you begin operations, not after. The cost of a thorough upfront analysis is a fraction of the cost of a post-commencement restructuring. Singapore rewards businesses that take compliance seriously. The US founders' tax guide we maintain at Adept Corporate Services addresses many of the specific questions North American operators face when entering the Singapore market.

— Wandy & Terence

How adept corporate services can help you

Adept Corporate Services works directly with North American business owners and corporate managers navigating Singapore's registration, tax, and compliance requirements. Whether you are establishing a new Singapore subsidiary, assessing your BEPS 2.0 exposure, or resolving a filing backlog with IRAS, the Adept team provides hands-on support without automated responses or generic templates.

Services include Singapore company registration, corporate secretarial compliance, tax filing, and advisory on entity structuring for foreign companies. Adept Corporate Services also supports bank account opening, payroll, and MAS licensing for funds and regulated entities. Contact the team directly to discuss your specific situation and get a clear picture of your obligations before your next filing deadline.

FAQ

Does singapore have CFC rules for foreign subsidiaries?

Singapore does not have CFC rules. Undistributed income in foreign subsidiaries is generally not subject to Singapore tax at the parent level, consistent with Singapore's territorial tax system.

What triggers a corporate income tax filing obligation in singapore?

A Singapore corporate income tax filing obligation is triggered by Singapore-sourced income or by management and control being exercised in Singapore. Incorporation or banking alone does not create a filing requirement.

Who is affected by singapore's multinational enterprise (minimum tax) act?

The Act applies to multinational enterprise groups with consolidated annual revenue of EUR 750 million or more in at least two of the four preceding fiscal years, starting from fiscal year 2025.

What is the difference between a singapore branch and a subsidiary for tax purposes?

A subsidiary is a separate Singapore tax resident entity eligible for startup exemptions and tax treaties. A branch is treated as an extension of the foreign parent and does not qualify for startup exemptions or the same treaty benefits.

Can IRAS penalize a foreign company for late tax filings?

IRAS issues estimated tax assessments for companies that fail to file on time, which typically result in higher tax liabilities than accurate self-reported figures, along with additional financial penalties.

Recommended

- Starting and Setting Up a Business or Company in Singapore | Adept Corporate Services

- New Register of Registrable Controllers (RORC) Filing Requirements from 16 June 2025 | Adept Corporate Services

- Singapore Single Family Office 2026 Guide | Adept Corporate Services

- Setting Up a Company in Singapore for a Foreigner: A Step-by-Step Guide | Adept Corporate Services