Managing a cross-border transaction with a Singapore entity is not as simple as wiring money and signing a contract. North American businesses routinely underestimate the regulatory complexity, payment friction, and reporting obligations that come with international business transactions involving Singapore. Between foreign entity compliance Singapore requirements, data protection rules, and multi-currency treasury challenges, the gap between "deal agreed" and "deal closed" can be wider than expected. This guide walks you through every stage, from compliance preparation to payment execution and audit readiness, so you can move faster and avoid the mistakes that cost businesses real money.

Table of Contents

- Key takeaways

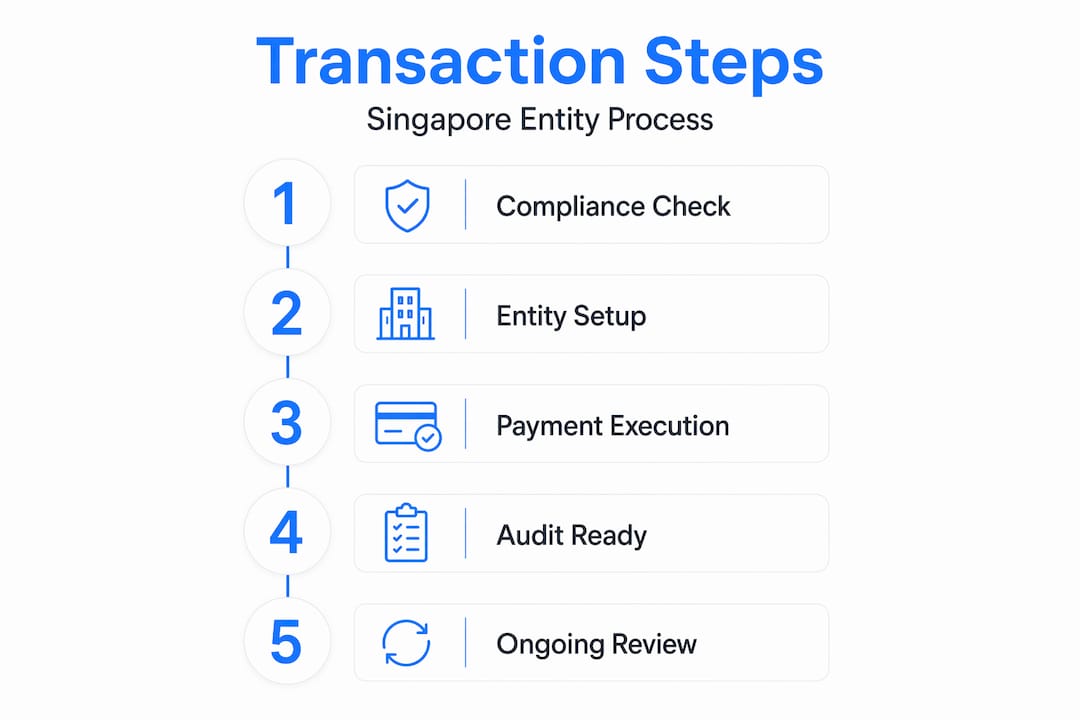

- Cross-border transaction Singapore entity: the compliance foundation

- Executing Singapore cross-border payments efficiently

- Financial reporting and audit readiness

- Verification and troubleshooting common issues

- My take on what actually determines success here

- How Adept-cs supports your Singapore transaction setup

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Compliance comes first | Audit your transaction structure for PDPA, FCPA, and FDI screening obligations before any funds move. |

| Payment costs are avoidable | Multi-currency accounts and faster payment rails can significantly reduce forex and transfer fee losses. |

| SFRS and IFRS are not identical | Consolidation adjustments for revenue recognition and FX translation are required for multinational groups. |

| Arbitration beats litigation | Build arbitration clauses into Singapore contracts from the start for faster, globally enforceable dispute resolution. |

| Early setup saves money | Establishing proper entity structures and treasury processes before transactions begin prevents costly corrections later. |

Cross-border transaction Singapore entity: the compliance foundation

Before any funds move or contracts are signed, you need a clear picture of the legal and regulatory environment. Singapore operates a 17% corporate tax rate and offers several entity structures relevant to foreign businesses, including private limited companies, representative offices, and branch offices. Each carries different liability profiles, tax treatment, and compliance obligations that directly affect how you structure overseas transaction regulations.

Foreign direct investment screening is a growing concern. 74% of deals are prevented from closing on time due to administrative issues, and 75% of senior dealmakers identify FDI screening as the primary risk in cross-border transactions. For North American businesses, this means entity formation timelines need to be built into deal schedules, not treated as an afterthought.

Data protection is another area where many businesses get caught off guard. Singapore's Personal Data Protection Act (PDPA) imposes a Transfer Limitation Obligation that requires any Singapore payment service provider or entity transferring personal data overseas to maintain PDPA-comparable protections through contractual and technical safeguards. If your transaction chain involves customer data flowing through multiple jurisdictions, you need documented data flow maps and signed data transfer agreements before you start.

Legal compliance goes beyond data. Routine transactions can trigger US Foreign Corrupt Practices Act (FCPA) violations or export control breaches without anyone noticing. A surgical audit of transaction DNA means reviewing the end-user, the payment route, the goods or services involved, and any intermediaries. This is not optional for businesses with US nexus.

- Review Singapore entity structure for tax and liability implications before transacting

- Confirm FDI screening requirements for your industry and transaction size

- Map all personal data flows and execute PDPA-compliant transfer agreements

- Audit for FCPA, export controls, and restricted end-user exposure

- Check the 2026 compliance calendar for Singapore-specific filing deadlines

Pro Tip: If you are acquiring or investing in a Singapore entity rather than simply transacting with one, engage a Singapore-qualified corporate services provider to run a compliance pre-check before the term sheet is signed. Fixing structural problems after the fact costs three to five times more than getting it right upfront.

Executing Singapore cross-border payments efficiently

Payment execution is where good deals go wrong. Payment inefficiencies cost Singapore merchants an estimated US$12 billion annually, and outbound cross-border payment volume in Asia-Pacific is projected to grow from $11.3 trillion in 2025 to $19.8 trillion by 2033. The opportunity is massive, but so is the cost of doing it poorly.

Here is a practical sequence for managing Singapore cross-border payments from North America:

- Open a multi-currency account. A Singapore-based multi-currency account lets you hold SGD, USD, and other currencies without converting on every transaction. This alone reduces forex drag significantly.

- Use faster payment rails where available. Singapore's PayNow system connects to regional networks including India's UPI and Thailand's PromptPay. For eligible transactions, faster payment linkages reduce settlement time from days to seconds.

- Compare payment corridors. Not all USD-to-SGD transfers are priced equally. Bank wire, fintech platforms, and licensed money changers each carry different FX spreads and transfer fees. Hidden costs in international transfers erode margins for SMEs more than most finance teams realize.

- Set rate alerts. SGD/USD exchange rates move within a managed float band set by the Monetary Authority of Singapore. Monitoring rate movements and timing larger transfers can yield meaningful savings on significant transaction volumes.

- Document payment instructions in writing. Singapore banks require clear beneficiary details, purpose codes, and sometimes supporting documentation for large transfers. Missing fields cause delays that compound across time zones.

| Payment method | Speed | Cost profile | Best use case |

|---|---|---|---|

| Bank wire (SWIFT) | 1-3 business days | Higher fees, wider FX spread | Large, infrequent transfers |

| Fintech platform | Same day to 1 day | Lower fees, tighter FX spread | Regular SME payments |

| PayNow (linked) | Near-instant | Low to no transfer fee | Smaller, frequent SGD payments |

| Multi-currency account | Instant (internal) | Minimal conversion cost | Treasury holding and netting |

Pro Tip: For businesses making recurring payments to a Singapore entity, consider setting up a Singapore corporate bank account through your local entity. This converts what would be cross-border transfers into domestic SGD transactions, removing SWIFT fees entirely on the Singapore side.

Financial reporting and audit readiness

This is the section most North American businesses skip until their auditors flag a problem. Singapore uses Singapore Financial Reporting Standards (SFRS/I), which are aligned with but not identical to IFRS. Consolidation adjustments are required for revenue recognition, FX translation, lease accounting under SFRS(I) 16, and transfer pricing between related entities.

For a US parent company reporting under US GAAP, the gap is even wider. Revenue recognition timing, lease capitalization thresholds, and financial instrument classification can all differ between your Singapore subsidiary and your US parent. These differences do not sort themselves out at year-end. They require ongoing reconciliation throughout the year.

| Reporting area | Singapore SFRS/I | US GAAP consideration |

|---|---|---|

| Revenue recognition | SFRS(I) 15, aligned with IFRS 15 | ASC 606, broadly similar but timing differences exist |

| Lease accounting | SFRS(I) 16, all leases on balance sheet | ASC 842, similar but threshold treatments differ |

| FX translation | Functional currency approach | ASC 830, broadly aligned |

| Transfer pricing | IRAS arm's length standard | IRS arm's length, documentation requirements differ |

Centralizing treasury functions in Singapore allows better scalability and regional financial reporting compared to decentralized models. Regional companies increasingly use Virtual CFO services to manage multi-entity consolidation and maintain audit-ready books across jurisdictions.

- Reconcile SFRS/I to your parent company's accounting framework quarterly, not annually

- Maintain a transfer pricing policy document before intra-group transactions begin

- Track functional currency designations for each Singapore entity separately

- Build audit trails for all intercompany loans, service fees, and royalty payments

Verification and troubleshooting common issues

Even well-prepared transactions run into problems. Knowing what to look for, and how to respond, separates businesses that close deals on time from those that spend months in remediation.

Entity formation delays are the most common source of friction. 90% of senior dealmakers expect cross-border M&A activity to increase despite these operational hurdles. Singapore company registration typically takes one to three business days for straightforward cases, but bank account opening can take four to eight weeks depending on the bank's due diligence requirements. Build this into your project timeline.

Payment delays often trace back to incomplete documentation rather than technical failures. Singapore banks require purpose-of-payment codes for inward remittances above certain thresholds. Missing or incorrect codes trigger manual reviews that can hold funds for five to ten business days.

For data protection compliance throughout complex payment chains, cross-border payment compliance requires detailed data flow mapping and strict contractual obligations at every handoff point. If your payment processor subcontracts to a third-party settlement network, your PDPA obligations follow that data downstream.

Dispute resolution strategy should be decided before a dispute arises, not after. Arbitration is preferred for cross-border enforceability because international conventions make awards enforceable across jurisdictions in ways that court judgments are not. Include an arbitration clause in every Singapore contract, specifying the Singapore International Arbitration Centre (SIAC) as the default forum.

Regulatory changes also require ongoing attention. Singapore's Monetary Authority of Singapore (MAS) updates payment service licensing requirements and AML/CFT obligations regularly. Contracts with Singapore entities should include a compliance review clause that allows either party to adjust terms when material regulatory changes occur.

My take on what actually determines success here

I've worked with dozens of North American businesses entering Singapore, and the pattern is consistent. The ones that struggle are not the ones with bad deals. They are the ones that treated compliance and treasury setup as administrative tasks to handle after the commercial terms were agreed.

What I've learned is that the regulatory complexity of a cross-border transaction with a Singapore entity is not a one-time hurdle. It is an ongoing operational requirement. PDPA obligations evolve. MAS licensing categories shift. Transfer pricing documentation requirements tighten. The businesses that build systems to monitor these changes from day one spend far less time and money than those who react to problems after they surface.

The other thing I see consistently underestimated is the value of audit-ready financial reporting from the start. A Singapore entity that cannot produce clean, reconciled financials on demand is a liability in any M&A, fundraising, or regulatory review. Getting your SFRS/I to GAAP reconciliation process right in year one is far cheaper than reconstructing two years of records under audit pressure.

My honest advice: treat your Singapore entity setup as a strategic infrastructure decision, not a paperwork exercise. The advantages of Singapore as a foreign business hub are real, but they only materialize if the underlying structure is built correctly.

— Terence

How Adept-cs supports your Singapore transaction setup

North American businesses managing their first cross-border transaction with a Singapore entity face a steep learning curve across company formation, banking, compliance, and financial reporting. Adept-cs handles all of it under one roof, with real people you can reach directly. No automated responses, no generic advice.

Adept-cs offers corporate treasury services for businesses that need centralized fund management and multi-entity reporting across jurisdictions. For businesses starting from scratch, the Singapore company registration service covers entity formation, corporate secretarial compliance, and bank account opening assistance. Ongoing support includes tax compliance services and corporate secretarial services to keep your Singapore entity audit-ready year-round. If you are ready to move from planning to execution, Adept-cs is the team that knows how to manage cross-border funds for foreign-owned Singapore entities.

FAQ

What is a cross-border transaction with a Singapore entity?

A cross-border transaction with a Singapore entity involves any financial, commercial, or investment activity between a foreign business and a Singapore-registered company, including payments, intercompany transfers, and equity investments. These transactions are subject to Singapore's regulatory framework, including MAS oversight, PDPA data protection rules, and IRAS tax requirements.

How long does it take to open a Singapore corporate bank account?

Singapore company registration typically completes in one to three business days, but corporate bank account opening takes four to eight weeks due to bank due diligence processes. Planning ahead and preparing complete documentation significantly reduces delays.

What are the PDPA obligations for cross-border payments involving Singapore?

Singapore's PDPA Transfer Limitation Obligation requires that any personal data transferred outside Singapore receives protection comparable to PDPA standards. This means payment service providers must implement contractual safeguards and technical controls at every point in the payment chain.

Why is arbitration recommended for Singapore cross-border contracts?

Arbitration is preferred because awards issued under international conventions are enforceable across jurisdictions in ways that court judgments typically are not. The Singapore International Arbitration Centre (SIAC) is widely recognized and provides a neutral, efficient forum for resolving international commercial disputes.

How do I align Singapore financial reporting with US GAAP?

Singapore uses SFRS/I, which is aligned with IFRS but not identical to US GAAP. Key differences exist in revenue recognition timing, lease accounting thresholds, and transfer pricing documentation. Quarterly reconciliation between SFRS/I and US GAAP, supported by a qualified Singapore accounting team, is the most effective approach.

Recommended

- U.S.–Singapore Free Trade Agreement (USSFTA) | Adept Corporate Services

- Starting and Setting Up a Business or Company in Singapore | Adept Corporate Services

- Setting Up a Company in Singapore for a Foreigner: A Step-by-Step Guide | Adept Corporate Services

- Singapore Single Family Office 2026 Guide | Adept Corporate Services